This article raises the issues for Trustees to consider when a charity is in financial stress/distress and highlights the potential consequences if the appropriate steps or advice is not taken and the Charity ultimately falls into insolvency.

This is the first in a series covering charities and the not-for-profit sector. A further article covering the practical measures that trustees can take to optimise cash and where the charity cannot continue what options are available, which is linked at the end of this article.

What is the ‘Insolvency Twilight Zone?’

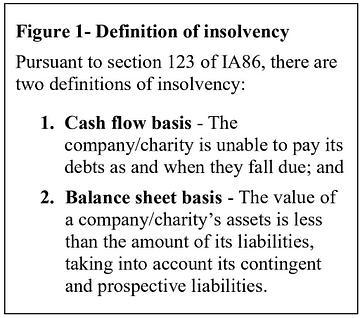

Trustees typically have a strong commitment and emotional involvement with the charity in which they are managing. However, many Trustees do not realise that their duties to the charity change during, and as the charity approaches, insolvency (see Figure 1). When a charity is (or is at risk of becoming) insolvent, the law prioritises the interests of all creditors to ensure they are not left out-of-pocket, and increases the accountability of trustees. Failing to protect creditors’ interests at the appropriate time can leave Trustees exposed personally for various claims from a future liquidator (see later).

The ‘insolvency twilight zone’ is that period where the charity is perhaps not quite at the stage of being unable to pay its debts as and when they fall due, but the Trustees consider that this could become a reality. At this time, the Trustee’s duties must shift away from the charitable objectives towards the creditors’ interests. Knowing when to make this switch is not straightforward and Trustees should promptly seek independent expert advice to protect themselves against claims being brought in the event of an insolvency.

What to do if the charity is approaching the ‘insolvency twilight zone’

i) Know your financial position

It is essential for Trustees to have up-to-date management information to have a full grasp on the charity’s financial position at any given time so that important decisions can be made readily. Having a good cash flow forecasting model which can be updated on a rolling thirteen-week period is vital for the management of the charity and, particularly where approaching the ‘insolvency twilight zone’, evidencing whether the charity is expected to be able to pay its debts as and when they fall due. Projecting income is a significant challenge and Trustees should always be prudent when making their assumptions.

Trustees should also scenario test their cash flow forecast to better understand cash sensitivities (e.g. the loss of a key donor). This also helps with managing the charity’s reserves as pinch points can be identified and additional funding released, where relevant.

It is important to recognise that, where a charity is facing insolvency, there are certain costs which tend to arise that may not ordinarily be included within the cash flow forecast of a going concern entity but must be considered where cash is limited and the charity could be wound down.

These costs include:

- Dilapidation claims in respect of leased property

- Termination charges for certain contracts

- Redundancy costs

- Certain run off costs if the charity is to wind down

- Professional fees including solicitors, insolvency practitioners, valuation agents & accountants.

It is recommended that charities seek advice to assist with the preparation of such information, where reserves are forecast to diminish.

ii) Trustees’ duties

Where it is determined that a charity is at risk of becoming insolvent and the creditors’ interests are to take precedence, the Trustees duties include:

- Only using charitable funds for the purposes relating to the objectives and the preservation of assets.

- Not repaying some creditors in favour of others. For example, paying a debt connected to the trustees, but no effort is made to make payments on other debts, could lead to a preference claim from a liquidator.

- Not selling-off the charity’s assets at lower than market values – Disposals should be at arm’s-length and through independent valuation agents.

- Not arranging for new and unaffordable lines of credit to be opened up – This includes increasing an overdrawn bank facility or making payments on credit cards.

Failure to adhere to any of the above could leave the Trustees open for claims from a future liquidator. It should be noted that claims can be brought against any Trustee who has been appointed within 3 years of the insolvency so resigning in times of distress does not provide any protection.

iii) Review the Charity’s governing documents

It is prudent to engage solicitors to review the charity’s constitution documents to avoid any potential issues further down the line, should an insolvency process become necessary. This is particularly relevant where the charity is unincorporated or takes an unconventional form, such as Royal Charter.

In our experience of dealing with some older charities, the trust deed can be difficult to interpret, particularly where it refers to closure of the charity and the distribution of residual assets. Also, with the passage of time, certain stipulations within the deed could become redundant. For example, on a recent care home matter, the London borough where the charity operated had changed as London had expanded over time, and it was necessary for an Order to be obtained from the Charity Commission for the funds to be distributed to the new, correct borough, for the same charitable use purposes.

iv) Regular review

Trustees should hold more frequent board meetings to assess the financial and operational landscape. Board minutes detailing the rationale for making decisions will be important to defend any claim for wrongful trading or misfeasance, should a liquidator bring such a claim.

What claims can be brought against the Trustees, should the charity enter an insolvency process?

Preferences (section 239 Insolvency Act 1986 (‘IA86’))

- Preference is where a creditor is put in a more beneficial position which is to the detriment of the Charity’s other creditors. The insolvency practitioner would need to prove ‘desire’ to put the creditor in a better position but where the beneficiary is connected to the Charity, such as a Trustee, desire is presumed. Trustees should be mindful that by electing to not pay a certain creditor (e.g. the defined pension scheme or a landlord) but maintaining other creditor payments, could also constitute a preference.

- If a preference is found to have been made, the Trustees could face personal liability for some or all of the Charity’s debts. The insolvency practitioner would apply to Court for the transactions to be set aside, and for recovery to be made against Trustees.

Transactions at Undervalue (‘TUV’) (section 238 IA86)

- This is where the charity has transferred or sold a charity asset to a third party for either a price that is considerably lower than its true value or, no payment at all. Where a charity enters into insolvency, the liquidator can go back two years or more from the date of insolvency and can apply to court to have the transaction(s) reversed.

- Where trustees have carried out TUVs, they could face other potential penalties other than personal liability such as a fine or criminal prosecution.

- There is a defence to this claim whereby the charity entered into the transaction in good faith and for the purpose of carrying on the charitable objectives and, at the time of the transaction, there were reasonable grounds for believing that it would benefit the charity.

Wrongful trading (section 214 IA86)

- Once a charity becomes or is likely to become insolvent, the trustees’ duties change to ensure creditors are protected. Wrongful trading is where the trustees of a charitable company allowed the company to trade at a time when they knew, or should have known, that it was, or would inevitably become, insolvent. The court, on an application from an insolvency practitioner, can impose a liability on a trustee to make a contribution to the Charity’s assets. Trustee Indemnity Insurance can be taken out to cover such a claim, provided the trustees acted in good faith.

- Some examples of behaviours or actions of wrongful trading include: not filing annual accounts, taking excessive salaries that the charity cannot afford, trading whilst insolvent, taking credit from suppliers when there was ‘no reasonable prospect’ of paying the creditor on time, wilfully piling up debt.

- The Government announced in March 2020 that, due to coronavirus, there has been a temporary suspension of wrongful trading provisions in the UK until 30 September 2020 to “remove the threat of personal liability” from directors/trustees. Trustees should note, despite this suspension, they are still open to personal claims for preferences, TUV and fraudulent trading in the same period.

Fraudulent trading (section 213 IA86)

- This is where the business of a charity is carried on with intent to defraud creditors and can be linked with the claims set out above. Fraudulent trading is a criminal offence and the punishments can be severe, including fines and imprisonment. Any person (not limited to Trustees) who were knowingly parties to carrying on the charity in a fraudulent manner are liable to make any contributions to the charity’s assets as a Court thinks proper. This claim cannot be covered by indemnity insurance, although some policies may cover defence costs of trustees found to be innocent.

Conclusion

Trustees will unlikely be penalised where they can show that, in the lead up to an insolvency, their reasonable and objective business decisions have been based on accurate financial information and with appropriate professional advice.

Whilst we have highlighted the risks and pitfalls for Trustees in this publication, there are a number of practical steps which they should take to avoid personal liability, even where the risk of the charity’s failure appears slight:

- Avoid increasing the charity’s debts as soon as you are aware that the company is or is likely to become insolvent.

- Take care when entering transactions which could give rise to a claim.

- Hold frequent Board Meetings and keep detailed minutes.

- Take prompt independent professional advice (accounting and legal).

- Ensure that the rights of the creditors take precedence over the charitable objectives once there is a perceived risk of insolvency.

- Treat all creditors equitably and do not ‘prefer’ one over another. This includes the payment of Trustees’ debts/expenses as to do so could cause complications for trustees personally in an insolvency.

- If not already in place, consider taking out Trustee Indemnity Insurance.

Our team has considerable experience in advising charities, not-for-profit organisation, and Trustees facing financial distress. Should you require any assistance, please contact Jonathan Reason. We are experts in this field and are here to help.

Click here to view Part 2 – Practical steps and options for Trustees of a distressed charity

Other articles

- Considering closing a solvent company? Act now, before tax advantages are downgraded in Labour’s Autumn Statement

- Press release – Noble Tree Foundation (In Administration)

- Practical steps and options for Trustees of a distressed charity

- The ‘Insolvency Twilight Zone’: Risks & pitfalls for Trustees in times of Charity Financial Distress

- CBW Recovery LLP achieves ACCA Approved Employer status